Contents

Overview

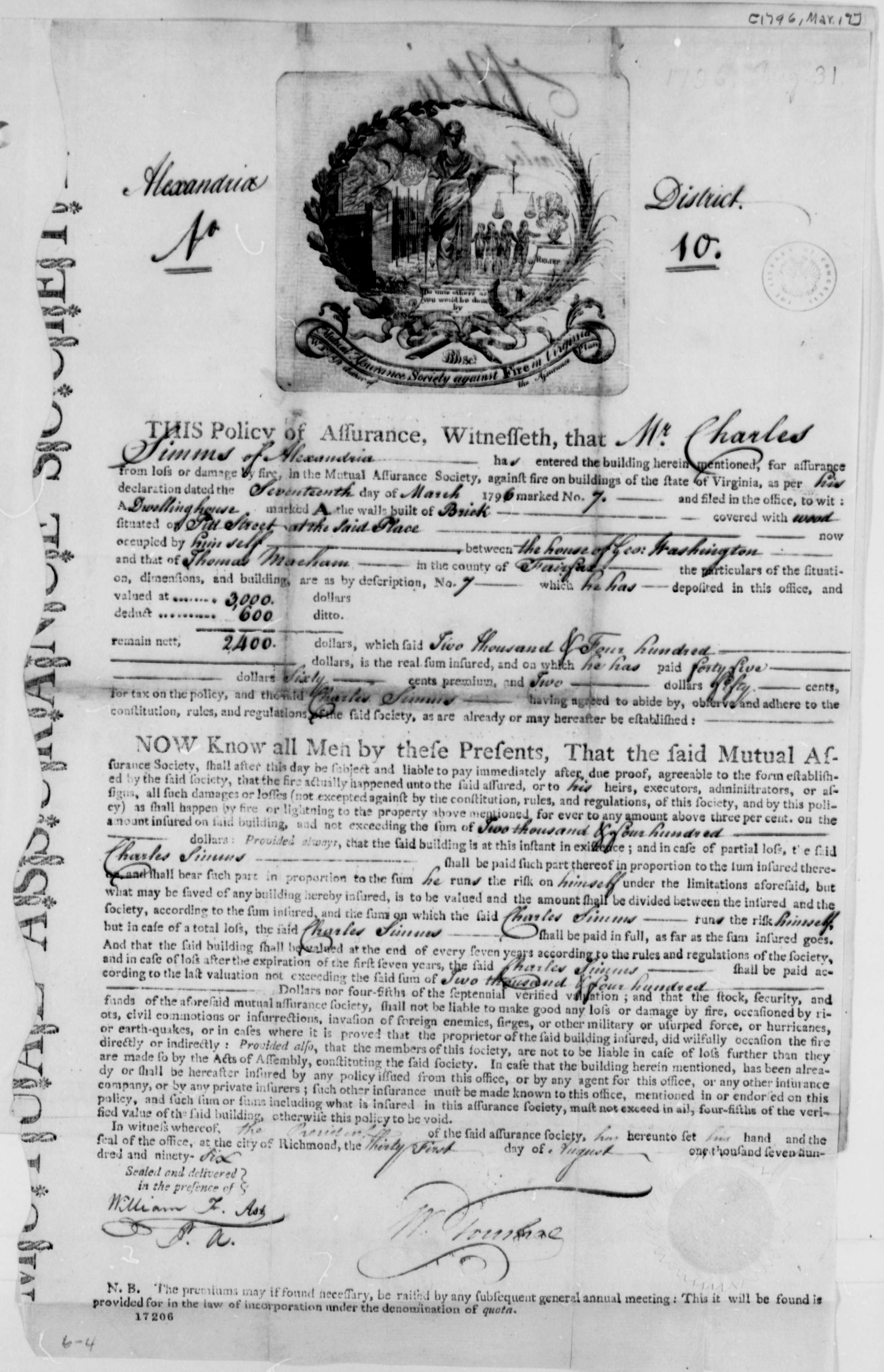

The concept of insurance policies traces its roots back to ancient maritime trade, where merchants pooled resources to cover losses from shipwrecks. Early forms of risk-sharing, like the Roman collegia (fraternal societies), provided mutual aid for funeral expenses and other misfortunes, laying groundwork for formal contracts. Modern insurance policies gained momentum in 17th-century London, particularly with the establishment of Lloyd's of London, which initially focused on marine insurance. By the 18th century, fire insurance policies became prevalent, driven by the increasing frequency of devastating urban fires. Life insurance policies, initially viewed with suspicion and often tied to gambling, began to mature with actuarial advancements, notably through the work of mathematicians like Edmond Halley and the founding of companies like the Equitable Life Assurance Society. The Industrial Revolution further spurred the need for diverse insurance policies, covering new risks associated with factories, machinery, and expanding transportation networks like railways.

⚙️ How It Works

At its core, an insurance policy functions as a risk transfer mechanism. The policyholder pays a premium, a predetermined fee, to the insurer. In return, the insurer commits to indemnify the policyholder for losses incurred due to specific events or perils outlined in the contract, such as fire, theft, illness, or death. The policy details the scope of coverage, including the sum insured, deductibles (the amount the policyholder pays before the insurer contributes), and exclusions (events or circumstances not covered). Policies are typically drafted as standard form contracts, meaning they use pre-written, standardized language to ensure consistency and efficiency, a practice pioneered by early insurers to manage administrative overhead. The insurer's obligation is legally binding, contingent on the policyholder fulfilling their end of the bargain, primarily by paying premiums and adhering to policy conditions, such as reporting claims promptly and accurately.

📊 Key Facts & Numbers

The global insurance market is a colossal economic force. Property and casualty insurance accounts for roughly half of this market, with life and health insurance making up the remainder. The insurance industry manages trillions of dollars in assets, making it a significant player in global financial markets.

👥 Key People & Organizations

Key figures in the evolution of insurance policies include Howard Kunreuther, a prominent researcher in risk management and disaster insurance, and George L. Head, a former president of the American Risk and Insurance Association who significantly contributed to insurance education. Major organizations like Lloyd's of London, established in 1688, and the Prudential Insurance Company of America have been instrumental in shaping the industry and developing diverse policy offerings. Regulatory bodies such as the National Association of Insurance Commissioners (NAIC) in the U.S. and the European Insurance and Occupational Pensions Authority (EIOPA) play critical roles in setting standards and ensuring the solvency and fairness of insurance providers. The International Actuarial Association also provides global guidance on actuarial practices essential for policy pricing and solvency.

🌍 Cultural Impact & Influence

Insurance policies have profoundly shaped societal norms around risk and security. They underpin the functioning of modern economies by enabling businesses to undertake ventures with predictable financial safeguards, fostering innovation and investment. The widespread availability of policies for health, life, and property has provided a crucial safety net for millions, reducing the devastating impact of personal tragedies and economic downturns. Public perception of insurance policies has evolved from skepticism to a fundamental expectation for financial planning. The language and structure of insurance contracts have also influenced legal drafting and contract law more broadly, emphasizing clarity, specificity, and the management of potential disputes. The concept of 'insurable interest'—the requirement that the policyholder must stand to suffer a financial loss if the insured event occurs—is a fundamental principle that has permeated various legal and financial domains.

⚡ Current State & Latest Developments

The insurance policy landscape is currently undergoing significant transformation, driven by technological advancements and evolving consumer expectations. The rise of insurtech startups is challenging traditional models with data analytics, artificial intelligence (AI), and blockchain technology to offer more personalized policies, streamline claims processing, and improve underwriting accuracy. For example, companies like Lemonade utilize AI to process claims in minutes. Telematics in auto insurance, using data from vehicle sensors, allows for usage-based pricing, a stark departure from traditional risk assessment. The increasing frequency and severity of climate-related disasters are also forcing insurers to re-evaluate risk models and policy terms, leading to discussions about affordability and availability of coverage in high-risk areas. The COVID-19 pandemic also highlighted gaps in coverage, particularly concerning business interruption and event cancellation policies, sparking debates about policy wording and regulatory intervention.

🤔 Controversies & Debates

Controversies surrounding insurance policies often center on claims disputes, premium increases, and the interpretation of policy language. Insurers have faced criticism for denying claims based on technicalities or alleged misrepresentations by policyholders, leading to protracted legal battles. The practice of 'underwriting' itself, where insurers assess risk and set premiums, can be contentious, with accusations of discriminatory pricing based on factors like race, socioeconomic status, or pre-existing health conditions, although many jurisdictions have regulations against such practices. The affordability of insurance, particularly for essential coverages like health and flood insurance in vulnerable regions, remains a persistent debate, with some arguing for greater government intervention or subsidies. Furthermore, the complexity of policy documents often leaves policyholders confused about their actual coverage, leading to unexpected financial burdens when claims are made.

🔮 Future Outlook & Predictions

The future of insurance policies is poised for greater personalization and automation. AI and machine learning will likely enable hyper-personalized policies tailored to individual behaviors and real-time risk assessments, moving away from broad risk pools. Blockchain technology holds the potential to enhance transparency, security, and efficiency in policy administration and claims processing, potentially reducing fraud and administrative costs. Parametric insurance, which pays out based on predefined triggers (e.g., earthquake magnitude, wind speed) rather than actual loss assessment, is expected to grow, particularly for natural disaster coverage. Insurers will increasingly grapple with the systemic risks posed by climate change, potentially leading to new forms of coverage or a greater reliance on public-private partnerships. The integration of IoT devices will provide continuous data streams for risk monitoring and prevention, blurring the lines between insurance and risk management services.

💡 Practical Applications

I

Key Facts

- Category

- finance

- Type

- topic